I remember looking at my brokerage account on a Tuesday afternoon and feeling a weird, hollow coldness in my chest. Everything was gone. Not just the "fun money," but the house down payment and the emergency fund I’d spent six years building. It’s a story I’ve seen repeated in Discord servers and Reddit threads a thousand times: the moment someone realizes that option credit spreads destroyed my life wasn't a sudden explosion, but a slow, confident walk into a trap.

Credit spreads are marketed as the "smart" way to trade. Financial influencers talk about them like they're a literal ATM. You sell an expensive option, buy a cheaper one to hedge it, and pocket the difference. High probability of profit, they say. Limited risk, they say.

The math looks foolproof. Until it isn't.

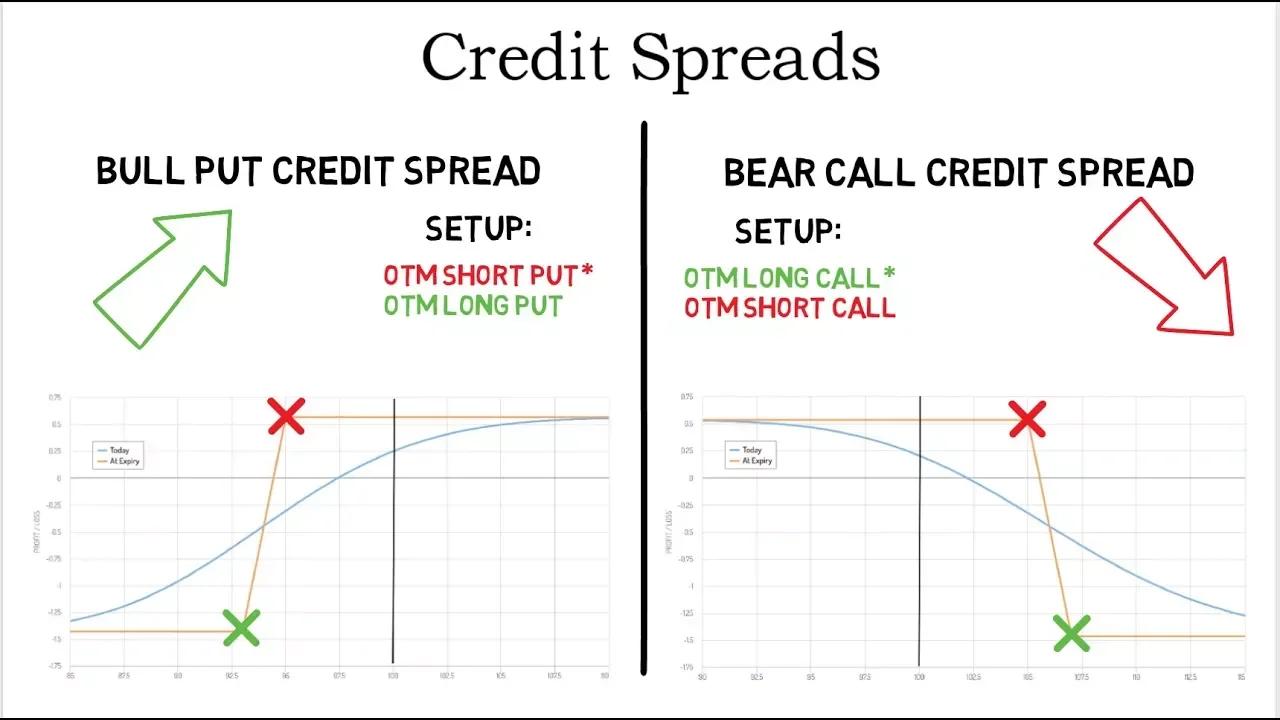

The Math of the "Penny Picker"

The fundamental problem with credit spreads—specifically bull put spreads or bear call spreads—is the risk-to-reward ratio. Most retail traders aim for a "high probability" trade, meaning they have a 80% or 90% chance of making money. To get those odds, you have to accept a tiny payout for a massive potential loss. You might risk $4,000 to make $400.

It feels great for three months. You win ten times in a row. You start thinking you’re a genius. You start sizing up.

Then, a "Black Swan" event hits. Or maybe just a regular, boring earnings miss. The stock gapped down 15% overnight. Because you were "defined risk," you thought you were safe. But when you’re trading spreads with high leverage, a single "max loss" event wipes out months—or years—of gains. People like Nassim Taleb, author of The Black Swan, have spent decades warning about this exact "picking up pennies in front of a steamroller" behavior. It works until the steamroller speeds up.

Why People Think Credit Spreads are Safe

The industry loves credit spreads because they generate massive commission volume and keep traders engaged. You’re told that because you have a "long" leg (the option you bought), your risk is capped. Technically, that’s true. If the stock goes to zero, you only lose the width of the spread.

But "limited risk" is a marketing term. It doesn't mean "low risk."

If you have $20,000 in your account and you open five spreads that each have a max loss of $4,000, you are technically at risk of total ruin. Most traders don't realize they are over-leveraged until a volatility spike hits. Volatility expansion (higher IV) makes spreads harder to close for a profit, even if the stock price stays relatively still. It’s a psychological meat grinder. You’re watching the "Unrealized P/L" turn deep red, and the "limited risk" doesn't feel very limited when it represents your entire net worth.

The Pin Risk Nightmare

There is a specific, terrifying technicality that leads to people saying option credit spreads destroyed my life, and it’s called Pin Risk.

Imagine you sold a spread that expires on Friday. The stock price is right in between your two strike prices at the closing bell. You think, "Cool, I only lost a little bit." You go to sleep.

Over the weekend, the person who bought the option you sold decides to "exercise" their right. Suddenly, you are on the hook for hundreds of shares of an expensive stock. But because it's Saturday, your "long" leg—the protection you bought—has already expired worthless. You are now "naked" a massive position you can't afford. If the stock gaps against you on Monday morning, you don't just lose your spread money. You might end up owing the brokerage hundreds of thousands of dollars.

This isn't a ghost story. It happened to numerous traders during the 2020 volatility spikes and the 2021 meme stock craze. Even modern platforms like Robinhood or Tastytrade can't always protect you from the mechanical realities of the Options Clearing Corporation (OCC).

The Psychological Toll of the "Slow Bleed"

It’s not always one big crash. For many, the destruction is incremental.

You lose $2,000. You try to "roll" the position to a later date to avoid the loss. Now you’re deeper in the hole. You double down to "average down" your entry. This is the Gambler’s Fallacy in action. Because credit spreads have such a high win rate, traders become addicted to the "win." They can't handle the ego hit of a loss.

When the losses finally outpace the wins, the mental health impact is devastating. Sleep goes first. Then the ability to focus at your "real" job. Relationships strain because you’re hiding the fact that the "safe" investment strategy just ate the vacation fund.

Realities of Professional Risk Management

Real professionals—the ones at firms like Susquehanna or Citadel—don't trade spreads the way YouTubers tell you to. They don't just "set it and forget it."

- Delta Neutrality: They are constantly hedging the directional risk.

- Gamma Risk: They rarely hold positions into the final week of expiration when things get "jumpy."

- Position Sizing: They might only risk 0.5% of their capital on a single trade. Retail traders often risk 20% or 30%.

How to Actually Protect Yourself

If you are currently in a hole or considering using credit spreads as a primary income source, you need a reality check. You cannot "income trade" your way to wealth without understanding the tail risk.

- Stop using more than 2% of your account per trade. If a max loss destroys your life, your position was too big. Period.

- Close trades at 50% profit. Don't squeeze the last nickel out of a spread. That’s when the risk is highest relative to the reward.

- Avoid Earnings. Trading spreads over earnings is pure gambling. The "Implied Volatility Crush" can help you, but the "Gap Risk" can end you.

- Always close before expiration Friday. Never, ever let a spread expire "close to the money." The risk of assignment is not worth the extra $20 in premium.

- Acknowledge the bias. We are currently in a market regime where "selling volatility" has been profitable. That doesn't mean it’s a law of physics. Markets change.

If you feel like your life is being ruined by your trading account, the most "expert" move you can make is to stop. Close the positions. Walk away. The market will be there in six months. Your sanity might not be if you keep trying to "win back" what the spreads took.

The goal of trading is to stay in the game. If your strategy has a "destroy my life" button hidden in the fine print, it’s not a strategy. It’s a ticking clock.